Blog Archive

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- February 2018

- January 2018

- December 2017

- November 2017

Categories

Why it pays to use your 2022/23 ISA allowance right now

Published: April 11, 2022 by Jennifer Armstrong

The 2022/23 tax year has only just started, but you should already start thinking about how you’ll use your allowances over the next 12 months. It can help maximise your assets.

In the 2022/23 tax year you can deposit up to £20,000 into ISAs. If you don’t use this allowance before the end of the tax year, you lose it. You can save or invest tax-efficiently through an ISA, so making full use of your allowance can help your money go further.

The period from February to the beginning of April is sometimes dubbed “ISA season” as savers and investors scramble to find the best rates to make use of their allowance before the end of a tax year.

If you left using your 2021/22 ISA allowance until the deadline was near, don’t let your ISA slip your mind now. It’s worth thinking about maximising it earlier in the 2022/23 tax year. Here’s why.

Drip-feeding your deposits can make your ISA goal part of your budget

If you want to maximise your ISA allowance or have a goal for how much you want to put in, making regular deposits a part of your budget can help.

Depositing £1,666 into your ISA each month can be more manageable than adding a lump sum at the end of the tax year. If you don’t have a lump sum to add to your ISA, breaking down your end goal can make sense.

It can help ensure that the money doesn’t get used to cover other expenses and keep you on track.

If you’re thinking about breaking down your ISA deposits over the year, setting up a standing order can simplify it.

In addition to making deposits more manageable, drip-feeding your money can be useful if you’ll be investing through an ISA.

Investment markets will rise and fall throughout the year. So, by spreading out deposits, you’ll be buying at different points throughout the market cycle. It’s an approach that can remove the temptation to try and time the markets.

Depositing a lump sum now means you have longer to earn interest or returns

If you already have a lump sum available to deposit, doing so now means you could have an extra 12 months of interest or returns than you would if you waited until April 2023.

If you’ll be saving through a Cash ISA, the extra interest added to your account over the year can really add up. Using your ISA allowance now can help you make the most of your money.

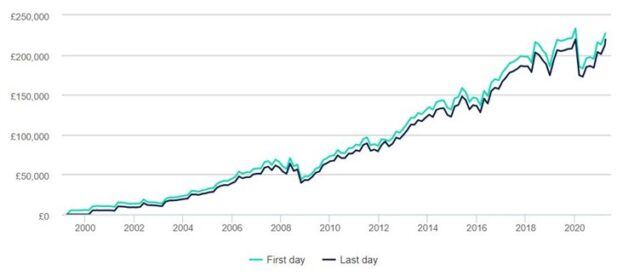

Adding a lump sum if you’ll be using a Stocks and Shares ISA to invest means you can potentially benefit from an additional 12 months of investment returns. The graph below shows how investing £5,000 each tax year delivers different returns if you invested on the first working day of the tax year compared to the last working day.

Source: Hargreaves Lansdown

While both options have done well and returned over 99% growth, you would be better off by investing at the start of the tax year overall.

However, you should keep in mind that investment performance cannot be guaranteed.

Some years, investing at the start of the tax year could mean you end up with less if investments perform poorly. You should consider your investment time frame and risk profile when making investment decisions and reviewing performance.

Should you save or invest through your ISA?

If you want to use your ISA allowance for the 2022/23 tax year now, you should think about whether a Cash ISA or a Stocks and Shares ISA is right for you.

A Cash ISA is a useful way to save. Your savings will benefit from interest, however, as the interest rate is likely to be lower than inflation, your savings may be losing value in real terms.

Over the long term, the effects of inflation add up. As a result, a Cash ISA may be right for you if you’re building an emergency fund or are saving for short-term goals.

If you’re putting money away with long-term goals in mind, a Stocks and Shares ISA may be appropriate.

Investing provides a chance for your wealth to grow at a pace that matches or exceeds inflation. But this cannot be guaranteed, and market volatility can mean investment values fall.

Investing for a longer period can smooth out the ups and downs. As a result, you should invest with a minimum time frame of five years.

As well as time frame, you should also assess which investments are right for you. All investments carry some risk and the decisions you make should reflect your wider financial circumstances.

Are you ready to think about how to maximise your ISA allowance for the 2022/23 tax year?

Please contact us to discuss your options and the steps you can take to help your money go further, including using your ISA and other allowances this tax year.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only. The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.