Blog Archive

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- February 2018

- January 2018

- December 2017

- November 2017

Categories

Landlords, rising interest rates could affect cash flow and your long-term plans

Published: September 1, 2022 by Jennifer ArmstrongIf you’re a landlord, your outgoings may have increased this year thanks to rising interest rates and could climb further. It’s essential that you review your cash flow and the effect it could have on long-term plans.

A combination of factors, including the Ukraine war and the after-effects of the Covid-19 pandemic, means inflation is high. In the 12 months to August 2022, inflation was 9.9%.

In response to this, the Bank of England (BoE) has increased its base interest rate several times. In August, the rate increased to 1.75% after the biggest hike in 27 years. If you took out a mortgage to purchase a buy-to-let property, your repayments are likely to rise.

How rising interest rates could affect your mortgage repayments

If you have a variable- or tracker-rate mortgage, your repayments may already have changed. If you have a fixed-rate mortgage, it’s likely your outgoings will increase when your current deal ends.

As most buy-to-let mortgages are interest-only, even a small increase to the rate could affect your outgoings and how profitable a property is.

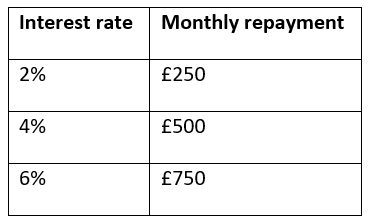

If you borrowed £150,000 through an interest-only mortgage, the below table demonstrates how changing interest rates would affect you.

Source: Money Saving Expert

The BoE expects inflation to peak at around 13%, and it’s likely to make further changes to the interest rate in the coming months.

As this could affect your outgoings significantly, you should review your cash flow. How much could your mortgage increase before the property is no longer profitable?

Research from estate agents Hamptons suggests that if mortgage rates reached 5.6%, the average buy-to-let would lose money.

With one of your largest outgoings predicted to rise further, you may consider increasing the rent to bridge the gap.

Zoopla statistics suggest this is something many landlords have already done. At the start of 2021, average annual rental growth reached a 14-year high, with average rents increasing by £88 a month when compared to a year earlier.

Make sure you speak to a local estate agent first, as demand for rental properties can vary across the country. An estate agent will provide a guide for the rental yield your property could achieve.

As well as affecting your cash flow now, higher mortgage costs could affect your long-term plans. For example, if you plan to use the income for retirement or use the profit to pay off the mortgage debt, you may now need to reassess.

2 other ways high inflation could affect landlords

It’s not just mortgage repayments that are being affected by high inflation. Here are two other areas you should consider as a landlord.

- Higher maintenance costs: At times, your property will need maintenance work carried out. In many cases, costs have increased for both materials and labour. So, if something needs repairing at your property, it’s now likely to cost more. Reviewing how you’d pay for necessary maintenance could highlight a gap as costs rise.

- Greater risk of arrears: Families are facing increased pressure on their budget and there’s a risk the economy could fall into a recession. As a result, there’s an increased chance that some tenants will be unable to pay their bills. If this happened, would your insurance cover arrears?

Could you secure a better mortgage deal?

If your mortgage deal is coming to an end, you may be able to secure a better deal.

Switching to a mortgage with a lower interest rate could save you money and mean that your buy-to-let property is more profitable.

There are lots of mortgage lenders to consider and it’s not just the interest rate you’ll pay that’s important. Depending on your circumstances, you may also want to consider the mortgage fee, term or flexibility.

If you’re ready to search for a new mortgage deal, please contact us. We’ll help you find the lenders that suit your needs and offer guidance throughout the application process, including explaining what the interest rate will mean for your repayments.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Buy-to-let (pure) and commercial mortgages are not regulated by the FCA.